When does a cash-out refinance make sense?

A cash-out refinance may be worth considering in Florida if:

- You are replacing higher-interest debt with lower-cost borrowing.

- You are funding home improvements that add value.

- Your new monthly payment still fits comfortably within your budget.

- You plan to stay in the property long enough to benefit.

When might it not be a good idea?

A cash-out refinance may not be ideal if:

- You only need a small amount of cash.

- The new loan significantly increases your monthly payment.

- You plan to sell the property soon.

- The total cost outweighs the benefit of the cash received.

How much cash can you take out in Florida?

The amount depends on your home value, current loan balance, loan type, and lender guidelines. Most programs limit how much equity you can access, especially for primary residences.

Will your monthly payment go up?

It depends. Some homeowners see higher payments due to a larger loan balance, while others offset this by restructuring the loan. The only reliable way to know is to compare scenarios.

Cash-out refinance vs HELOC

A cash-out refinance replaces your existing mortgage. A HELOC is a separate credit line secured by your home. The better option depends on how much you need, how you plan to use it, and your long-term plans.

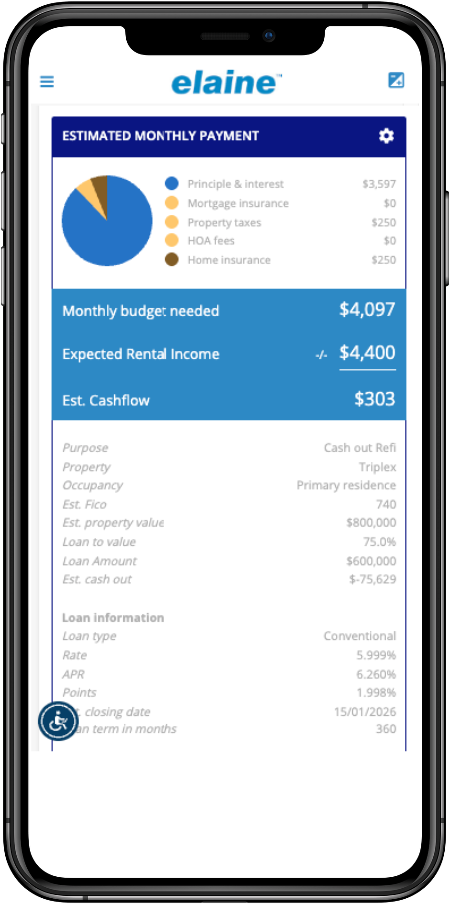

See real numbers, not estimates

Compare your payment, cash-out, and loan structure instantly.